How Inflation Impacts Pension Plans in Retirement

5 minutes

Quick Answer: Inflation affects pension plans by reducing the future purchasing power of fixed monthly payments. If your pension has no cost-of-living adjustment (COLA), your income may stay the same while housing, food, healthcare, transportation, and other costs rise. Inflation can also influence interest rates, which may affect lump-sum pension payout values.

Inflation and Your Pension

A monthly pension may feel stable, but if it does not include a cost-of-living adjustment, the same payment may buy less each year. Inflation reduces purchasing power of fixed pension payments over time, and it can influence interest rates which can affect lump-sum pension payouts. For retirees reliant on pensions, COLAs can be a valuable part of your retirement plan.

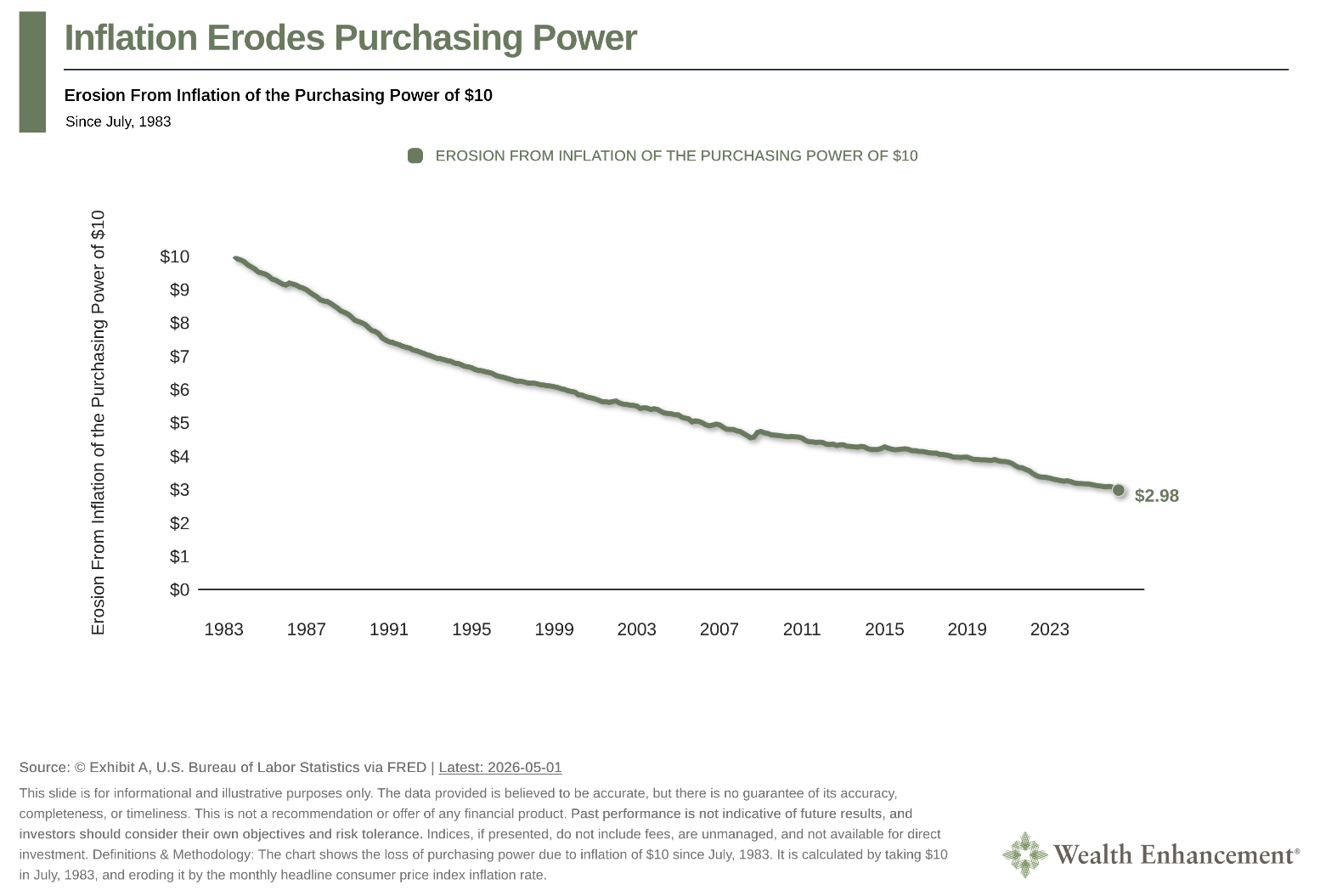

According to the US Bureau of Labor Statistics (BLS), the Consumer Price Index for All Urban Consumers (CPI-U) rose 4.2% from May 2025 to May 2026, which means your money buys 4.2% less. Luckily, a COLA can help your pension keep up with inflation.

Chart: How Inflation Impacts Your Purchasing Power Over Time

What Type of Pension Do You Have?

Defined Benefit Pension Plans

Defined benefit pension plans usually promise a fixed monthly benefit based on a formula, often tied to years of service, age, and compensation.

Lump-Sum Pension Payouts

Lump-sum pension plans allow retirees to take a one-time sum of their pension instead of lifetime monthly payments.

Pension Annuity Payments

Pension annuities are a type of defined benefit pension plan. Annuities are offered by insurance companies where you make payments to the company so you can receive income later in life. The income you receive does account for interest rates, meaning your money can increase in value. In fixed annuity plans, there is a set interest rate for the term of the annuity. In variable annuity plans, your money is put into market-based investments like stocks and bonds. As the value of your investment appreciates or depreciates, so does your payout.

Annuity payouts have several options, including:

- Life only payouts. These payouts allow the annuitant to receive payments until they pass away.

- Joint and survivor payouts. The annuitant and joint annuitant receive payments, and after the passing of one annuitant their partner will receive payments for as long as they’re alive.

- Period certain payouts. The annuitant receives payments over a set period. If they pass during that period, the payments go to their beneficiaries.

Why Fixed Pension Payments Lose Purchasing Power

If a retiree receives $5,000 per month and inflation averages 3% per year, the payment still says $5,000 on the check, but its real spending power declines over time unless the pension includes a COLA.

What $5,000 Monthly Income May Feel Like Over Time

| Time | Year 1 | Year 5 | Year 10 | Year 15 |

|---|---|---|---|---|

| 2% inflation | $60,000 | $55,430.73 | $50,205.32 | $45,472.50 |

| 3% inflation | $60,000 | $53,309.22 | $45,985.00 | $39,667.07 |

| 4% inflation | $60,000 | $51,288.25 | $42,155.20 | $34,648.50 |

Does Your Pension Include a Cost-of-Living Adjustment?

What is a Pension COLA?

A cost-of-living adjustment (COLA) is designed to help benefits keep pace with rising prices. A COLA includes an inflation rate with your payments. Often COLAs are capped at a 2% inflation rate, but they can still help restore your purchasing power.

Why COLAs Can Change the Pension Decision

A fixed $5,000 monthly pension with no COLA will erode from $60,000 of spending power of in your first year to $45,472.50 in your 15th year, assuming an average of 2% inflation.

Lump sum pensions often do not include COLAs as you receive the entire sum of money at once.

Note: At first, your pension with a COLA may be less than a fixed sum payment, but as inflation increases, so does the benefit of your COLA.

Pension COLA vs Social Security COLA

Social Security has an annual COLA mechanism that has a set annual inflation rate. For 2026, the rate was 2.8%. Pension COLAs depend on plan terms and often do not change despite interest rates rising or falling.

How Inflation and Interest Rates Can Affect Lump-Sum Pension Payouts

Why Higher Interest Rates Can Reduce Lump Sums

Your lump sum is an estimated value of future pension payments. While it does account for some inflation, it is not an accurate predictor of the markets. When inflation rates rise more than your lump sum calculated, the value of future payments generally falls.

Why Timing Can Matter

Plans may update calculations monthly, quarterly, or annually. If you choose to get your payout while calculations are low, it can mean losing money in the long run. For example, with a 3% interest rate, a $5,000 monthly pension benefit over 20 years would result in approximately a $901,555 lump sum payout. With a 6% interest, that lump sum payout decreases to $697,904.

Your payout value will depend on multiple factors including plan terms, age, IRS rates, and calculation timing. If you elect to get a lump sum payout plan, request the written calculation rules.

Lump Sum vs Monthly Pension: Which Handles Inflation Better?

| Option | Inflation protection | Income stability | Investment control |

|---|---|---|---|

| Monthly pension without COLA | None | Offers consistent income | Funds are not invested |

| Monthly pension with COLA | Includes inflation adjustment | Offers consistent income | Funds are not invested |

| Lump sum rollover to IRA | Minimal inflation protection | Offers one time payment | Allows funds to be invested |

| Joint-and-survivor pension | Depends on plan | Offers consistent income | Depends on plan |

| Life only pension | Depends on plan | Offers consistent income | Depends on plan |

| Option | Tax planning flexibility | Spouse or beneficiary impact | Main risk |

|---|---|---|---|

| Monthly pension without COLA | Can be tax exempt | Depends on plan | Inflation causes value of payouts to decrease over time |

| Monthly pension with COLA | Can be tax exempt | Depends on plan | May not keep up with cost of living |

| Lump sum rollover to IRA | IRA allows for some flexibility, but income taxes are likely | Depends on plan | Markets can cause the value of the payout to shift |

| Joint-and-survivor pension | Can be tax exempt | Allows spouse to claim benefits during life and after one spouse’s death | Often has lower monthly payouts |

| Life only pension | Can be tax exempt | Spouses and beneficiaries do not receive payouts | Offers no benefits to spouses and beneficiaries, also can be liable to inflation costs |

Other Factors That Should Influence Your Pension Decision

Apart from inflation and payout schedule, there are several other factors to consider when deciding on a pension plan, including:

- Your essential expenses. When planning for retirement, see how much your fixed costs would be covered by pension income and how much is covered by other sources.

- Spouse and survivor benefits. A life-only pension will provide higher monthly payments but will not provide benefits to your spouse or beneficiaries. Decide what benefits you should prioritize.

- Investment risk and discipline. A lump sum requires a plan for asset allocation, withdrawals, taxes, and market volatility.

- Employer and plan stability. The Pension Benefit Guaranty Corporation helps retirees manage their pension plan. Certain plan guarantees are subject to legal limits and protections.

Pension Inflation Planning Checklist

- Does my pension include a COLA?

- Is the COLA fixed, capped, partial, or CPI-based?

- How often is my lump-sum value recalculated?

- Which interest rates does the plan use?

- What survivor options are available?

- How much monthly income does my spouse need if I die first?

- What happens if I take the lump sum and invest it?

- Can I roll the lump sum directly into an IRA?

- What tax impact would a cash distribution create?

- How does this choice affect my estate plan?

- How much of essential spending is already covered?

- What inflation assumption is used in my retirement plan?

Strategies to Help Protect Retirement Income from Inflation

Aside from COLAs, there are several strategies to help combat inflation regardless of your pension plan, including:

- Build an inflation-aware withdrawal plan. Plan portfolio withdrawals and cash flow management while accounting for inflation.

- Maintain growth exposure where appropriate. Diversified investments and equities can grow with inflation rates, gaining value over time.

- Consider treasury inflation-protected securities. TIPS include a fixed rate of interest, and the principal of the TIPS can change allowing for greater protection against inflation.

- Coordinate pension, Social Security, and portfolio income. Create a well-rounded retirement income plan with multiple streams of income.

When to Get Professional Guidance

Pension plans are often irreversible and should be reviewed alongside taxes, investments, estate planning, and other retirement planning considerations. Before choosing a lump sum or monthly pension, speak with an advisor at Wealth Enhancement who can model how the decision fits into your full retirement income plan.

Frequently Asked Questions About Inflation and Pension Plans

How does inflation affect a pension?

Inflation reduces the purchasing power of fixed pension payments. If your monthly benefit does not increase, the same dollar amount may cover fewer expenses over time.

Do pensions increase with inflation?

Some pensions include cost-of-living adjustments, but many do not. Check your plan document to see whether your benefit has a COLA, how it is calculated, and whether it is capped.

Is it better to take a lump sum or monthly pension during inflation?

It depends on your plan terms, COLA, health, benefit needs, tax situation, and retirement income plan. A monthly pension may offer stability, while a lump sum may offer flexibility and legacy planning.

Why do interest rates affect pension lump sums?

A lump sum represents the present value of future payments. When interest rates used in the calculation rise, the lump sum value generally falls.

Are pension payments protected if my employer fails?

In many cases, yes. A direct rollover may avoid immediate taxation, but the money will generally be taxed later when distributed from the IRA.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. This article was originally published 9/28/2022 and has been updated.

2026-13263

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.