Editor’s Note: The below investment commentary was written prior to the attacks in Israel and therefore does not include comments on the increased geopolitical risk and market impacts. As the situation is changing rapidly, we will provide additional updates in subsequent commentaries.

Executive Summary

U.S. equity markets pulled back further in September as longer-dated Treasury yields rose. Markets repriced for interest rates staying higher for longer as 10-year Treasury yields rose to levels that haven’t been seen since 2007.

What Piqued Our Interest

Shutdowns, strikes and student loans were top of mind in September, all while markets adjusted to the prospect of interest rates staying near current levels for longer than expected. Despite the recent strength in economic data, concerns increased throughout the month as investors contemplated how these headline issues would negatively impact the economy in the fourth quarter.

First, the U.S. government narrowly avoided a shutdown on October 1, as a temporary funding bill was signed by President Biden, extending funding for federal agencies through November 17, 2023. However, the Speaker of the House, Kevin McCarthy, was ousted, and the uncertainty left by his vacancy has led to turmoil in Washington, as well as in the markets.

Second, the United Auto Worker’s strike began during the month and involved three unionized automakers in the U.S.: Ford Motor Company, General Motors, and Stellantis (maker of Chrysler and Dodge). These three automakers’ factories employ about 145,000 UAW members and produce about half of the vehicles manufactured in the United States, accounting for approximately 1.5% of annual GDP.

Lastly, we have known that student loan payments would resume in October, and it has been estimated by Goldman Sachs that these payments would subtract -0.5% from annualized GDP growth in the fourth quarter. The resumption of payments in full would be equal to roughly $70 Billion, or around 0.3% of disposable personal income.

Despite these headline-making events, the most pressing issue for investors has been the rapid rise in the 10-year Treasury yield, increasing by approximately 100 basis points, from 3.8% to 4.8% in the last three months. The 10-year Treasury yield is often considered to be the risk-free rate, the rate at which you can slowly and conservatively grow your money over time, and it’s used to discount future cash flows in order to calculate a net present value. The higher the discount rate, the lower the net present value.

Economic growth concerns for the fourth quarter may be warranted, but at the same time, it is what we all need to bring inflation back down to more normalized levels. The labor markets likely hold the key in determining whether the Fed will hike once more in November or December, and it won’t simply be focused on the unemployment rate, as wage growth, the number of job openings, and labor participation rates will also be scrutinized. Lastly, the labor market will also determine how long interest rates stay at these elevated levels, bringing attention and focus to each month’s jobs reports.

Market Recap

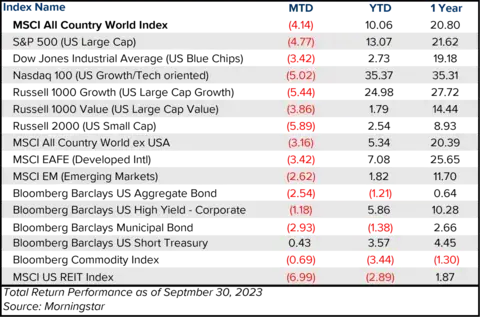

September is notoriously a weak month for markets. The S&P 500 Index has lost an average of -1.1% in September, dating back to 1928. This year was no exception, as markets pulled back further after declining in August. The S&P 500 Index fell -4.8% in September and is down -8% from its high in July. The pullback in equity markets was fairly consistent across the major U.S. indices, with the Tech-heavy Nasdaq 100 declining slightly more, down -5.0% for the month, while the blue chip Dow Jones Industrial Average declined slightly less, down -3.4%. Interest rate-sensitive areas, such as U.S. Small Caps (down -5.9%) and U.S. REITs (down -7.0%) fell the most as longer-term yields rose. International markets were down but not quite as much as U.S. markets, with the MSCI EAFE Index down -3.4% and Emerging Markets down -2.6%.

Fixed income declined once again, as the Bloomberg Barclays U.S. Aggregate Bond Index declined for a fifth month in a row, taking the year-to-date return into negative territory. The 10-year Treasury yield closed the month at 4.6%, a level not seen since 2007. Short-term Treasuries, as measured by the Bloomberg Barclays U.S. Short Treasury Index, held their ground and were up 0.4% for the month, thanks to the lower duration of shorter maturities. High-yield Corporate bonds had been having a strong year but fell -1.2% in September. Municipal bonds were down -2.9% and are now down -1.4% for the year.

Closing Thoughts

Interest rates, inflation, and labor markets remain the primary focus of market participants as we head into Q4. With interest rates at levels not seen since 2007, financial conditions continue to tighten as investments that were lucrative when interest rates were near zero are less attractive or cost prohibitive in a higher-rate environment. Economic strength, despite these tighter conditions, seems incongruous, which implies that economic growth will either slow from here or we’ll end up with the “soft landing” scenario that has gained so much steam this year. Markets are repricing for the probabilities of these outcomes on a daily basis. However, it is important to remember to stay the course so that gains accrue in the long run.

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.